Brady lists give officers a scarlet letter with no opportunity to appeal.

I left this comment on another place and thought I’d share it here. I was responding to an American pal – whom I normally agree with – who said the the UK’s vote for independence outside the EU was a disaster. I have jazzed it up a bit and added links. Well, it is Christmas!

The EU has become an increasingly regulated, bureaucratic entity, and while the UK tried to pull it in a different direction, the sclerosis of the continent got worse. The Single Market and “freedom of movement” aspect had their positives – up to a point. The Customs Union (external tariff wall, in other words) was a clear negative, however.

The structure of the EU is hostile to classical liberal economics in the medium term, not a plus.

The bureaucratic mission creep of the European Commission, unhampered by a largely toothless E. Parliament (it cannot initiate or repeal directives), meant the EU economy decelerated, imperceptibly at first. Its share of global GDP has shrunk and not just because other, non-European countries such as China and India have grown over the past few decades. While some of the reasons for Brexit were grounded in nationalism, which I dislike, some reasons were more classically liberal. Those reasons should not be discounted. Another point: for far too many, the ideas of free enterprise and freedom of trade became entwined, in a poisonous way, with the creation of transnational, bureaucratic structures distant from ordinary people. To that extent, the EU is part of the problem for those making the case for capitalism and open markets. When you say those words, far too many think of men and women in suits in Brussels regulating this and that, not entrepreneurship, trade and human interaction. That’s a problem.

For Americans reading this, remember that when the original 13 colonies broke free from the UK in the 1770s, they did so in part for reasons around representative government and the powers to tax with legitimate power. The EU increasingly came to the point where member states were reduced to regions of a centralising state.

Ross Clark’s Far From EUtopia is a marvellous read about Brexit, what went wrong, and more.

Britain is like an alcoholic who has spent a decade reassuring himself that, despite his binges and blackouts, he is “high functioning”. The reality is, however, that he is increasingly not actually functioning at all. We are headed for the rock bottom we so badly need. The moment of clarity is coming. It will be painful. But it’s the only thing that can save this country.

– Konstantin Kisin (£)

Amid the screams and pandemonium, one man stood tall: Ahmed al-Ahmed, a 43-year-old Syrian-born Muslim Australian and father of two.

Video footage, now viral across the globe, captures his instinctive charge, wrestling a firearm from one assailant, disarming him despite the peril. Injured but unyielding, al-Ahmed’s actions halted the rampage’s escalation, saving untold lives in that sun-kissed haven turned hellscape. Hailed as a hero by officials worldwide, his bravery bridges divides: Jewish donors have rallied to raise $1.3 million via GoFundMe for his recovery, praising his “selfless, instinctive, and undeniably heroic actions.” In a world fractured by suspicion, here is unity forged in fire. Award this man the George Cross, the Commonwealth’s pinnacle of civilian gallantry, let it gleam as a beacon for all who dare to protect the innocent.

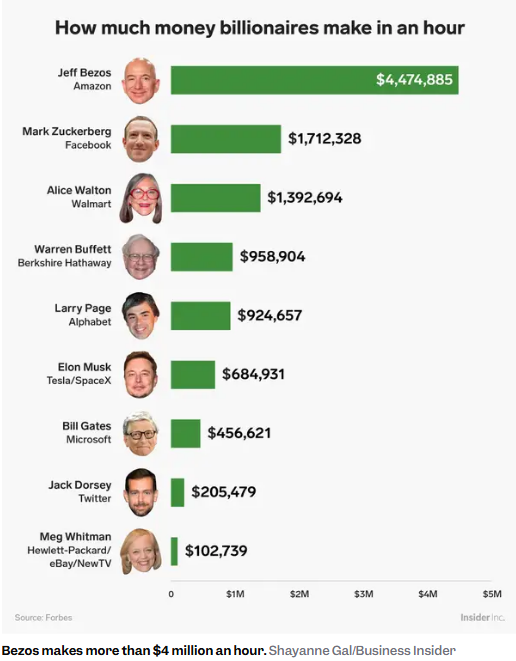

Every few months a headline or social media post circulates declaring that a corporate leader earns hundreds or even thousands of times more than the typical employee, and recent examples are no exception: Costco’s outgoing CEO reportedly made 336 times the median worker’s pay (less than Walmart or Target), McDonald’s CEO earned more than 1,224 times the median McDonald’s worker, Starbucks’s CEO took in an eye-popping 6,666 times the median Starbucks employee, and Jeff Bezos — by one viral estimate — earns in a single hour what a minimum-wage worker would take nearly 3.8 million hours, or roughly 434 years, to earn.

The implication is clear: such a ratio (if correct, which in many cases is questionable) is self-evidently immoral, wasteful, or economically harmful. Yet the CEO-to-worker multiple survives largely because it is a noisy rhetorical device, not because it withstands the most superficial levels of analytical scrutiny. As an economic metric, it is close to meaningless. As a guide to policy, it actively misleads.

The first flaw appears in the basic concept of the argument. Flatly: a worker’s pay and an executive’s pay are not two points on the same labor-market spectrum. They reflect two entirely different markets. The average employee is hired under conditions of broad substitutability — many people can competently perform the role with modest training. The CEO labor market is the opposite: extremely small, specialized, global, and contingent on track records that can shift a firm’s valuation by billions of dollars. The demand curve for top executive talent is steep; the supply curve is extraordinarily thin. This mismatch — not a moral failure — explains why compensation packages at the top sometimes reach what seem like astronomical numbers. A ratio comparing two unrelated labor markets tells us no more about fairness than comparing the salary of a cardiothoracic surgeon to that of a street performer.

The second flaw is arithmetic. Corporate executive pay is lumpy, frequently dominated by one-time stock grants or option awards tied to multiyear performance horizons. The ratio spikes not when the CEO receives a paycheck, but when an accounting rule requires the entire grant to be reported in a single year. Meanwhile, the denominator of that equation, the “average worker,” is sensitive to workforce composition. The hiring of more entry-level fulfillment workers, arrival of seasonal help, or divestment of a highly paid engineering division will cause ratio shifts by hundreds of points without a single change in executive pay. Treating that figure as a meaningful indicator is akin to using a funhouse mirror as a diagnostic tool.

Such a ratio also ignores value creation. Skilled executives can influence strategy, capital allocation, risk management, and organizational culture in ways that affect firm performance far more than incremental labor inputs elsewhere in the organization, even if the latter are voluminous. If a CEO’s decisions add even a few percentage points to long-term returns, the economic value created dwarfs the compensation. A $50 billion company that achieves a 2 percent valuation boost due to executive decisions has effectively created $1 billion in shareholder value; paying $20 million for that outcome is not just defensible but eminently rational, economically speaking. The relevant question is not “Is the ratio of worker to executive pay too large?” but rather “Does the CEO create more value than their talent costs?”

Executive-worker compensation ratios additionally elide market context. Firms compete globally for leadership talent. If US companies dramatically compressed pay at the top for any reason, the outcome would not be a sudden eruption of egalitarian harmony. It would be an exodus of top performers to private equity, venture capital, sovereign-wealth platforms, or foreign competitors willing to pay market rates. Pretending that either talent is immobile or that the corporate executive labor market will remain unchanged in the face of engineered political caps, ignores basic economics.

Most important of all, though, the ratio is a political cudgel. It bundles legitimate concerns, like stagnant productivity-adjusted wages, rising housing costs, and diminishing purchasing power into a single emotional statistic that points to the wrong culprit. If the goal is broad-based prosperity, the target should be the structural barriers and interventionist hijinks that hinder workers’ ability to climb the wage ladder: occupational licensing, restrictive zoning, limited labor mobility, regulatory frictions, and the inflationary biases that dampen entrepreneurial entry and tinker with money. Fixing those improves both growth potential and current station; punishing firms for hiring world-class leaders achieves neither.

Like so many poorly-conceived, interventionist policy proposals, the empty-headed ratio functions primarily as comparison, aiming not to build broader prosperity, but to yank down whomever stands taller. The “pay ratio” approach may animate headlines, but provides a poor basis for economic analysis and a worse benchmark for public policy. Sound economics demand far better metrics and clearer understandings of how value is created in modern firms.

Ultimately, broad judgments based on headline figures obscure the actual complexity of compensation structures, the competitive environments in which firms operate, and the incentives that drive investment, innovation, and growth. If the objective is to understand what contributes to a company’s long-term success — and how prosperity is generated and shared — then analysis must move beyond surface-level comparisons and toward more substantive measures of productivity, market conditions, and enterprise performance. Only then can the public debate shift from emotive comparison to genuinely constructive economic insight.